7-8% rates are bad by recent standards but not awful by historical standards. Depending on where I move and how much house I can get, I’d be willing to give up my 2.9% rate for something in that range.

There are a few other factors to consider right now, anyway. I’m a Houston resident, and this is supposed to be a particularly bad hurricane season along with a historic heat wave. My wife is terrified of the state’s newest right wing legislative push, as well. Michigan, Minnesota, and Washington is looking better and better as Texas brains are poisoned by MAGA media. And, despite having a gangbusters growth, my O&G employer decided to cut our bonuses from last year - so I’ve got one eye on the job market again. Our water bill jumped by 9% in a single year. Our interior roadways are falling apart, with no sign that the city or state plans to clean them up or improve access to public transit. HISD is being cannibalized by the governor’s cronies, so I won’t have anywhere to send my kids in a few years.

Would I pay an extra $500/mo to live in a state that isn’t run by pedophiles, bigots, and zealots? Absolutely. Bonus points if it got me out of the concrete jungle and put me in spitting distance of some decent mass transit.

If those are your problems with your area then you might as well just leave the US, we’re not getting mass transit anytime soon, climate change will make weather and necessities more expensive everywhere, and fascists are one lucky election away from bringing forth Gilead

A lot of Texans are thinking about it. My mother is deeply a-political, she retired last year, but she told me a year ago that if I needed to move to the Netherlands she would move to help me. (Her grandparents were dutch immigrants, so she might qualify for citizenship where I wouldn’t.)

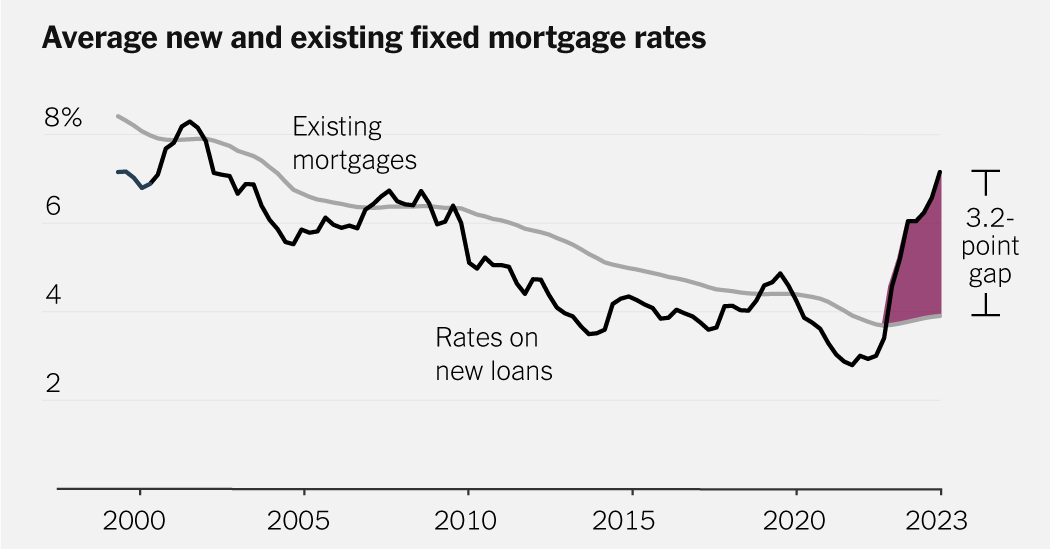

It will likely never get to 4% again unless there is another major recession or you are willing to get an ARM. Historically, 4% is extremely rare for fixed rate mortgages.

I suspect when rates go down, there will be a new rush for people wanting to change properties. That means new high demand for houses and another jump in valuation.

3.6 here (bought 22) and not fucking moving until rates are at least below 4 again. If that means I don’t ever move again then so be it

Either this is a typo or very dramatic lol.

deleted by creator

Typo but a funny one lol

7-8% rates are bad by recent standards but not awful by historical standards. Depending on where I move and how much house I can get, I’d be willing to give up my 2.9% rate for something in that range.

There are a few other factors to consider right now, anyway. I’m a Houston resident, and this is supposed to be a particularly bad hurricane season along with a historic heat wave. My wife is terrified of the state’s newest right wing legislative push, as well. Michigan, Minnesota, and Washington is looking better and better as Texas brains are poisoned by MAGA media. And, despite having a gangbusters growth, my O&G employer decided to cut our bonuses from last year - so I’ve got one eye on the job market again. Our water bill jumped by 9% in a single year. Our interior roadways are falling apart, with no sign that the city or state plans to clean them up or improve access to public transit. HISD is being cannibalized by the governor’s cronies, so I won’t have anywhere to send my kids in a few years.

Would I pay an extra $500/mo to live in a state that isn’t run by pedophiles, bigots, and zealots? Absolutely. Bonus points if it got me out of the concrete jungle and put me in spitting distance of some decent mass transit.

If those are your problems with your area then you might as well just leave the US, we’re not getting mass transit anytime soon, climate change will make weather and necessities more expensive everywhere, and fascists are one lucky election away from bringing forth Gilead

A lot of Texans are thinking about it. My mother is deeply a-political, she retired last year, but she told me a year ago that if I needed to move to the Netherlands she would move to help me. (Her grandparents were dutch immigrants, so she might qualify for citizenship where I wouldn’t.)

It will likely never get to 4% again unless there is another major recession or you are willing to get an ARM. Historically, 4% is extremely rare for fixed rate mortgages.

So they say but I’m 30 and have seen it twice already so…

Well, it happened in 2008 and 2020, so all we gotta do is wait for the economic crash in 2032 and we’ll be set!

The math checks out…

I suspect when rates go down, there will be a new rush for people wanting to change properties. That means new high demand for houses and another jump in valuation.